Pharmaceutical spending in the United States has reached a level that commands the attention of everyone from Capitol Hill to the kitchen table. According to data published by the Centers for Medicare and Medicaid Services, national spending on prescription drugs has consistently outpaced general medical inflation for more than a decade, placing it among the fastest-growing categories of personal health expenditure.

Against that backdrop, pharmaceutical companies were expected to raise prices on at least 350 drugs heading into 2026, a figure that exceeded the number of increases announced at the same point in the prior year. For millions of Americans, this trajectory is not an abstract policy concern. It is a monthly calculation made at the pharmacy counter.

The system that determines what a patient pays for a prescription is not a single structure but a layered web of private insurance plans, federal benefit programs, pharmacy benefit managers, manufacturer rebates, and government-imposed price controls.

Understanding how pharmaceutical payment, costs, and coverage interact requires looking at each of these components individually and then understanding how they function together, sometimes in alignment and sometimes in tension. A drug’s list price, the price negotiated by an insurer, the rebate a manufacturer pays back to a plan sponsor, and the final out-of-pocket amount a patient is charged can all differ substantially from one another.

The year 2025 marked a genuine inflection point. The federal government moved on multiple fronts simultaneously, from executive orders directing most-favored-nation pricing strategies to proposed mandatory payment models under the Centers for Medicare and Medicaid Innovation. Thirty-one states passed nearly 70 bills targeting drug costs within a single legislative year. The regulatory architecture shaping pharmaceutical payment is more active and more contested than it has been at any point in the past two decades. What follows is a factual account of how that system is structured, what it costs patients and payers, and how current and anticipated reforms are reshaping the terrain.

How Pharmaceutical Pricing Actually Works

The Gap Between List Price and What Anyone Pays

The sticker price on a prescription drug, known as the Wholesale Acquisition Cost, rarely reflects what any single payer actually pays. Manufacturers set that list price and then negotiate confidential rebates and discounts with pharmacy benefit managers, insurers, and government programs.

The PBM, acting as an intermediary between manufacturers and health plans, collects those rebates and may or may not pass the savings on to plan members or employers. This architecture has been central to ongoing federal and state scrutiny because it creates a situation where high list prices can generate larger rebate dollars while leaving patients, who often pay cost-sharing based on that list price, exposed to costs that do not reflect the negotiated reality experienced by their insurer.

Researchers at the USC Schaeffer Center for Health Policy found that net prices for branded drugs, after accounting for all rebates and discounts, have grown far more slowly than list prices in recent years.

Yet because many insurance plans structure cost-sharing as a percentage of list price rather than net price, patients in high-deductible plans or those in coverage gaps can still face significant out-of-pocket exposure even for drugs with heavily negotiated net costs.

The Role of Pharmacy Benefit Managers

Pharmacy benefit managers were originally created to administer prescription drug benefits on behalf of health insurers and employers. Over time, their role expanded dramatically. The three largest PBMs now control an estimated 80% of prescription claims processing in the United States. Their influence over formulary design, which drugs are covered and at what tier, gives them considerable power over both manufacturer pricing strategies and what patients pay.

States have taken direct aim at this structure. By the end of the third quarter of 2025, state legislatures had enacted dozens of PBM reform measures, including requirements for spread pricing transparency, restrictions on clawback fees charged to independent pharmacies, and prohibitions on certain steering practices. These reforms acknowledge that reducing administrative costs and opacity in the drug supply chain can lower what patients and employers ultimately pay, even without changing the manufacturer’s price.

Federal Coverage Programs and What They Pay

Medicare Part D: The New Out-of-Pocket Cap

Medicare Part D, the federal program providing prescription drug coverage to seniors and certain disabled individuals, underwent its most significant structural change in decades with the implementation of a $2,000 annual out-of-pocket cap beginning in 2025.

Before this change, Part D beneficiaries faced uncapped spending in the catastrophic coverage phase, meaning those with high drug costs could pay tens of thousands of dollars annually before the government stepped in. The cap, established under the Inflation Reduction Act of 2022, directly limits catastrophic spending exposure for the more than 50 million Americans enrolled in Part D.

Alongside the cap, the IRA restructured how cost-sharing liability is distributed among manufacturers, plan sponsors, and the federal government in the catastrophic phase. Manufacturers of drugs whose prices increase faster than inflation are now subject to rebates paid to the federal government, introducing a built-in financial incentive against excessive price growth for drugs used by Medicare beneficiaries.

Medicare Drug Price Negotiation

The most structurally consequential element of the Inflation Reduction Act was the authorization for the Department of Health and Human Services to directly negotiate drug prices with manufacturers for the first time in Medicare’s history. CMS published negotiated prices for an initial set of ten high-expenditure drugs under Medicare Part D, with those prices taking effect for the 2026 plan year. The program is set to expand annually, covering additional drugs under both Part D and Part B in future cycles.

This negotiation program has faced legal challenges from several pharmaceutical manufacturers arguing that mandatory negotiation constitutes an unconstitutional taking. Federal courts have largely sustained the program to date, though litigation is ongoing. The practical effect for patients enrolled in Medicare plans using the negotiated prices is a meaningful reduction in cost-sharing obligations for some of the most expensive and widely used medications.

Medicaid: State-Federal Cost-Sharing and Rebate Programs

Medicaid, which provides coverage to low-income individuals and families, already operates under a mandatory rebate system requiring manufacturers to pay the federal government a rebate equal to at least 23.1% of the average manufacturer price for most drugs, with additional inflation-based penalties. Because Medicaid covers more than 90 million Americans, it represents a substantial portion of the pharmaceutical market volume, and its rebate structure has long functioned as a de facto pricing floor for the industry.

States are exploring ways to expand on these existing rebate mechanisms. Proposals under discussion in several state legislatures would extend Medicaid-style rebate requirements to drugs purchased for state employee benefit plans, effectively using the purchasing power of state government workers as a second lever alongside the Medicaid program itself. Brookings Institution research has highlighted the potential savings available from broadening inflation rebate requirements beyond the current Medicaid context.

The Federal Policy Push in 2025 and 2026

Executive Action and the Most-Favored-Nation Framework

In April 2025, the Trump administration issued an executive order directing federal agencies to pursue a most-favored-nation pricing strategy under which Medicare would pay no more for drugs than the lowest price paid by economically comparable countries. Subsequent announcements included specific agreements to lower the cost of two of the most widely prescribed medications in the country, Ozempic and Wegovy, through this pricing framework.

Most-favored-nation pricing, sometimes called international reference pricing, has been debated in US policy circles for years. The core argument is straightforward: American patients and taxpayers pay substantially more for the same branded drugs than patients in Western Europe, Canada, Japan, and Australia, often without a clear corresponding benefit in terms of access or outcomes.

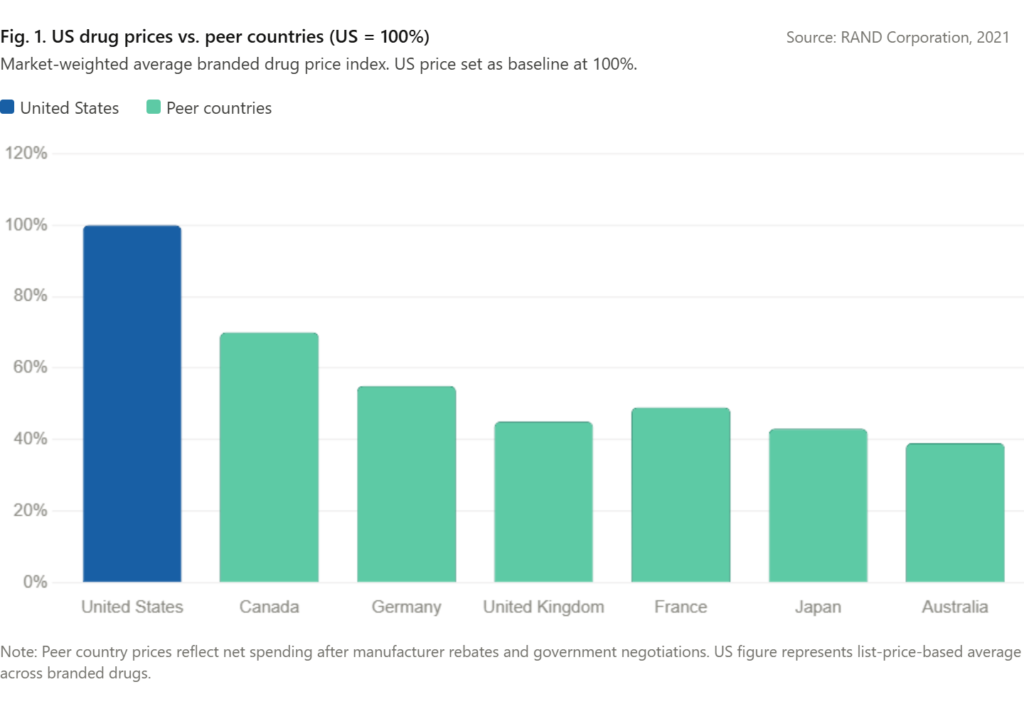

A 2021 RAND Corporation study estimated that US drug prices were roughly 256% of prices in 32 other countries on a market-weighted basis. The MFN framework attempts to close that gap by tying what Medicare pays to the prices achieved in those comparable markets.

The GLOBE and GUARD Models

Toward the end of 2025, the Centers for Medicare and Medicaid Innovation proposed two mandatory payment models with significant implications for pharmaceutical reimbursement. The Global Benchmark for Efficient Drug Pricing, or GLOBE Model, would apply to certain drugs reimbursed under Medicare Part B, which covers physician-administered drugs such as infusions and injections.

If a drug’s price exceeds what comparable countries pay, manufacturers would owe a rebate to the federal government. The mandatory nature of the model, covering all eligible Part B drugs rather than a voluntary subset, distinguishes it from earlier demonstration models.

The Guarding US Medicare Against Drug Costs, or GUARD Model, similarly uses international reference pricing benchmarks to calculate a price ceiling and requires manufacturers to pay rebates when the Medicare net price exceeds the benchmark. Taken together, these two models would, if finalized and implemented, represent the most ambitious use of international reference pricing in Medicare’s history.

Bipartisan Congressional Legislation

In May 2025, a bipartisan group of senators introduced legislation that would prohibit pharmaceutical manufacturers from charging higher prices in the United States than in peer countries. The bill drew support across party lines in a political environment where few issues command bipartisan consensus, signaling the degree to which drug pricing has become a priority that transcends typical ideological boundaries. The legislative vehicle, if enacted, would formalize through statute what the executive branch has attempted through executive action and regulatory models.

State-Level Action: A Policy Laboratory

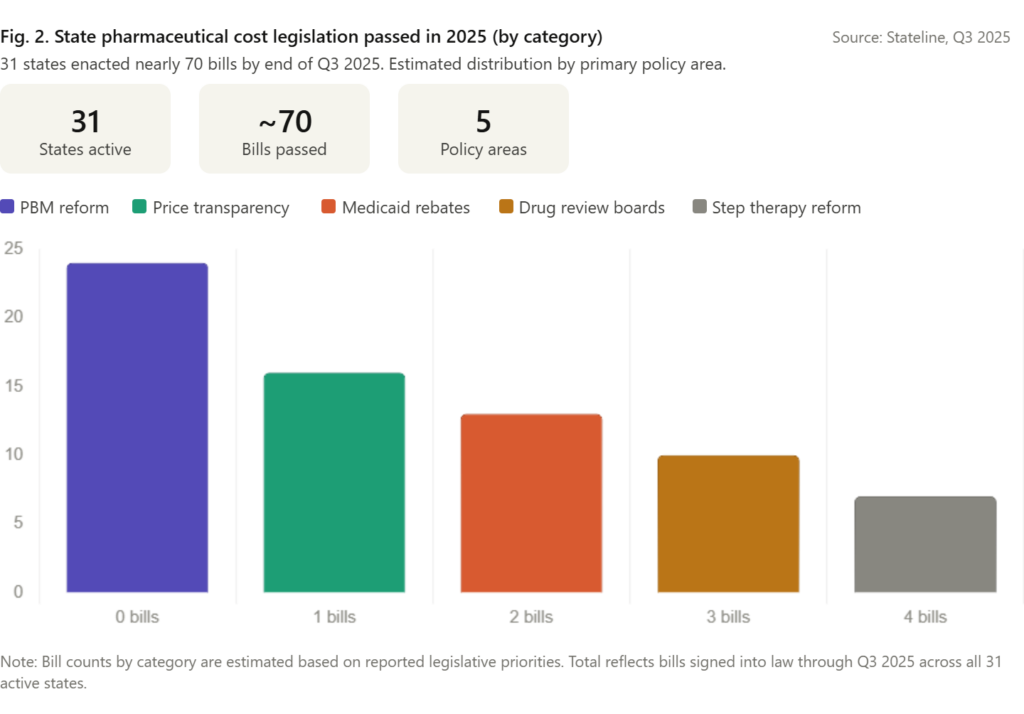

States have not waited for federal resolution of the pricing debate. By the close of the third quarter of 2025, 31 states had enacted nearly 70 pieces of legislation addressing prescription drug costs. The scope of these measures reflects the breadth of the problem as experienced at the state level.

Governors and legislators are accountable to constituents who face cost pressures at the pharmacy, state Medicaid directors managing budgets strained by high-cost specialty drugs, and state employee benefit fund managers trying to control premiums for government workers.

The tools available to states are more constrained than those available to the federal government. The Commerce Clause of the US Constitution limits a state’s ability to regulate pharmaceutical transactions that occur across state lines, which means that direct price controls on commercial drug sales face significant legal exposure. However, states retain considerable authority over programs they fund and administer, including their Medicaid programs, state employee benefit plans, and regulated insurance markets.

Drug pricing review boards, modeled on structures used in other countries to assess cost-effectiveness before coverage decisions, have been established in a growing number of states. These boards do not set prices directly but can recommend coverage limits or preferred alternatives, creating indirect pricing pressure on manufacturers who wish to maintain formulary placement.

PBM reform has proven politically viable across states with otherwise divergent healthcare policy approaches. Requiring transparent reporting of spread pricing, capping fees charged to independent pharmacies, and restricting certain rebate arrangements are reforms that have attracted support from rural legislators worried about pharmacy closures as much as from progressive health advocates worried about patient affordability. This breadth of coalition support has made PBM reform among the most durable and widely enacted categories of drug cost legislation at the state level.

Insurance Coverage Design and Patient Out-of-Pocket Costs

How Formularies Shape Access and Cost

Health insurance coverage for prescription drugs is structured around a formulary, a tiered list of covered medications. Drugs placed on higher formulary tiers generally carry higher cost-sharing requirements for patients, in the form of larger copayments or coinsurance percentages. Manufacturers seek favorable formulary placement through rebate negotiations with PBMs and plan sponsors. The result is that coverage decisions and patient cost exposure are shaped by factors that include but are not limited to clinical evidence.

Step therapy protocols, which require patients to try less expensive alternatives before a plan will cover a higher-cost drug, are a common formulary management tool. These protocols can reduce spending for payers but can also delay access to the most clinically appropriate therapy for individual patients. A growing number of states have enacted step therapy reform laws requiring exception processes for patients for whom the mandated sequence is clinically inappropriate.

The Special Challenge of Specialty Drugs

Specialty drugs, broadly defined as high-cost agents used to treat complex or rare conditions, represent a disproportionate share of pharmaceutical spending. Specialty drugs accounted for roughly 50% of total drug spending in the United States in recent years, despite representing a small fraction of total prescription volume. Biologics, gene therapies, and targeted oncology agents dominate this category.

Biosimilar competition has begun to put downward pressure on prices for some biologic drugs, with the entry of multiple biosimilars for adalimumab products providing one of the most closely watched examples. However, uptake of biosimilars has been slower than some analysts projected, in part because of PBM formulary design and in part because of existing patient assistance and rebate arrangements that have made the transition less economically straightforward for payers.

The Road Ahead: What 2026 Looks Like

The pharmaceutical cost and coverage landscape entering 2026 is one of genuine policy momentum but also substantial uncertainty. Federal regulatory models are proposed but not yet finalized. Litigation against core provisions of the IRA’s negotiation program continues.

State legislative sessions will produce additional bills in the same areas that proved active in 2025, and expanded rebate programs and further PBM reforms are likely areas of growth. Ozempic and Wegovy, the GLP-1 drugs that have become central to treatment conversations around type 2 diabetes and obesity, will remain in focus both because of their extraordinary utilization growth and because the federal pricing agreements announced in 2025 have made them a visible marker of what the MFN framework can achieve.

For patients, the near-term experience will be shaped by how quickly negotiated Medicare prices translate into lower cost-sharing at the point of sale, whether employer-sponsored plans adopt similar pricing disciplines, and how effectively state PBM reforms reduce administrative overhead in the supply chain.

For policymakers, the core challenge remains the same one that has defined American drug policy for generations: how to preserve incentives for pharmaceutical innovation while ensuring that the products of that innovation are accessible and affordable to the population that ultimately funds it through premiums, taxes, and out-of-pocket payments.

The policy activity of 2025 represents the most intensive effort in decades to shift that balance. Whether it succeeds will be measurable, in part, at the pharmacy counter.

Frequently Asked Questions

1. Why are prescription drug prices so much higher in the United States than in other countries?

US drug prices are higher primarily because the federal government, unlike those in most peer countries, historically has not negotiated drug prices on behalf of the national market. Manufacturers set prices without a centralized counterparty, and private insurers negotiate discounts individually. The IRA’s Medicare negotiation program represents the first significant change to this dynamic.

2. What is a pharmacy benefit manager, and how does it affect what patients pay?

A pharmacy benefit manager is an intermediary company that processes prescription drug claims on behalf of health plans and negotiates rebates from drug manufacturers. The rebates collected by PBMs may not be fully passed through to patients, meaning patients can pay cost-sharing based on a list price that does not reflect the discounts their insurer has already received.

3. What does the $2,000 Medicare Part D out-of-pocket cap mean for beneficiaries?

Starting in 2025, Medicare Part D enrollees pay no more than $2,000 out of pocket annually for covered prescription drugs. Before this change, there was no cap, and some beneficiaries with high drug needs paid far more. The cap provides meaningful financial protection for the roughly 1.5 million Part D enrollees who were previously spending above that threshold each year.

4. What is international reference pricing, and how would it lower drug costs?

International reference pricing ties what a government program pays for a drug to the price paid by comparable countries. Because countries with national health systems negotiate prices centrally, they generally pay substantially less for the same drugs. Anchoring US Medicare reimbursement to those benchmarks would reduce what the program spends and, potentially, what patients pay in cost-sharing.

5. Can states legally regulate drug prices?

States face constitutional constraints under the Commerce Clause that limit their ability to regulate drug prices for transactions crossing state lines. However, states retain full authority over the pricing terms of their own purchases, including Medicaid and state employee benefit programs. They also regulate insurance markets and PBMs operating within their borders, giving them indirect tools to address cost.

6. What is a formulary, and why does it matter for drug coverage?

A formulary is the official list of prescription drugs covered by an insurance plan, organized into tiers that determine how much the patient pays. Higher-tier drugs cost patients more at the pharmacy. Formulary placement decisions, often driven by rebate negotiations, directly determine patient access and affordability for specific medications.

7. What are biosimilars, and how do they affect pharmaceutical costs?

Biosimilars are versions of biologic drugs that have been shown to have no clinically meaningful differences from the original branded product. They typically enter the market at a discount to the original product. Greater biosimilar uptake has the potential to reduce spending significantly, as seen with the multiple biosimilars approved for adalimumab (marketed as Humira). However, PBM formulary decisions have slowed the pace of savings realization in some cases.

8. How does Medicaid control the prices it pays for drugs?

Medicaid operates under a mandatory rebate system in which manufacturers must provide rebates as a condition of coverage. Rebates are set at a minimum percentage of the average manufacturer price, with additional penalties when prices rise faster than inflation. These statutory rebates, combined with state supplemental rebate negotiations, make Medicaid one of the largest and most price-disciplined pharmaceutical purchasers in the country.

9. What is step therapy, and when can patients request an exception?

Step therapy is a coverage protocol that requires a patient to try and fail on less expensive drugs before the insurance plan will cover a higher-cost option. Patients can generally request a step therapy exception when they have already tried the required drugs and failed, when those drugs are contraindicated, or when a clinician documents that starting with the preferred therapy would be harmful. Many states have enacted laws mandating that insurers have clear and timely exception processes.

10. Will the drug pricing reforms of 2025 actually lower costs for the average patient?

The near-term impact varies significantly by coverage type. Medicare Part D enrollees benefit directly from the $2,000 cap and from negotiated prices on specific drugs. Those in employer-sponsored commercial plans will see changes more gradually, as reforms filter through PBM contract renegotiations and formulary updates. State PBM reforms may reduce administrative costs and improve pharmacy reimbursement, but the degree to which those savings reach patients depends on how plan sponsors pass them through. The reforms represent structural changes that should lower costs over time, though the pace and distribution of those savings remain uncertain.